When you make a purchase, you have to decide how to pay - should you use cash, a debit card, or a credit card? Each method has it's pros and cons...

- Cash is accepted everywhere, so having some hidden in your wallet is nice to have in case of an emergency.

- Some find using cash is a great way to limit spending - they find it psychologically harder to part with cash than to swipe a card. (Studies have shown that consumers who use cash are less likely to make impulse purchases.)

- Some business owners are willing to give you a discount when you pay with cash.

- For many people, the envelope method, which uses cash, is a great way to stick to a budget.

- Sticking to a strictly cash payment system ensures you won't fall into a debt trap. Once the cash is gone, you're done spending.

- When you make debit or credit purchases, even for a small amount, retailers are charged a transaction fee. This doesn't happen with cash. (This is why many small business owners have a minimum purchase requirement for credit and debit cards.)

There are cons to using cash, which include:

- No tracking. Anyone who's started the week with $100, and ended with $5 and only a vague sense of where the rest went, has learned this lesson.

- No protection. Many credit and debit companies offer limited protections on purchases made using their card.

- No rewards, such as cash back or travel miles, offered by many card companies.

- Purchases made with cash won't have an effect on your credit score.

- If you plan to make large purchases - such as buying a house or new car - using only cash, you'll need to follow a strict savings plan, which can be difficult.

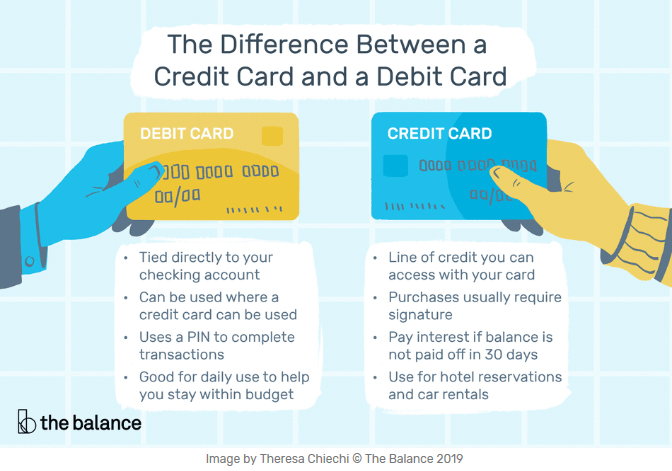

Debit and credit cards have similar features. Generally, both have the logo of a major credit card company (usually Visa© or MasterCard©), and both can be swiped to purchase goods and services.

The primary difference is where the money is drawn from when a purchase is made. Debit cards draw money directly from the buyer's checking account. A credit purchase is basically a loan - it's charged to a line of credit that must be paid back.

While debit and credit cards are quite similar, the differences are important.

Debit Cards

Debit cards are tied to deposits - generally checking accounts. When you swipe a debit card, the funds to pay for your purchase are automatically transferred from your account to the seller's account.

Pros:

- Easy access to cash. In addition to the nearly 500,000 ATMs in the US, many retailers offer cash back when you make a debit purchase.

- You can easily track your spending. Transactions generally show up immediately on your account ledger.

- It's easy to get a debit card - there are no credit checks, and using a debit card has no effect on your credit score.

- Making debit purchases won't put you in debt, making it harder to spend money you don't have.

- If your debit card is stolen, the Federal Trade Commission has set limits for the extent of your liability, which increase over time.

Cons:

- It's possible to overdraw your checking account, exposing yourself to fees that can add up quickly.

- On the other hand, debit purchases are sometimes declined, which can be embarrassing.

- If your debit card is used fraudulently it can tie up your funds, or even overdraw your account until your bank knows to disable your card.

Credit Cards

When you receive a credit card, it means you've been approved for a line of credit up to a certain amount (your credit limit.) When you pay for purchases with a credit card, the funds are transferred to the seller from your lender, who will then charge you for those funds.

Pros:

- Like a debit card, credit transactions make it easy to monitor your spending.

- Most credit cards allow you to access cash by taking out a cash advance, however there are usually fees associated with this service.

- Credit cards offer valuable protections, which vary by card. Typical protections include extended product warranties, price protections, replacing stolen/damaged items, and if you travel, things like travel insurance and luggage protection.

- Many credit card companies offer reward programs that can be quite beneficial.

- Responsible use of credit cards help to build your credit score, which can effect everything from your insurance rates to employment opportunities. Of course, the opposite is also true.

Cons:

- Credit cards make it easy to spend money that you don't actually have.

- If you don't pay your balance in full each month, you'll be charged interest and fees that can add up quickly.

The bottom line is there's no one correct answer for all circumstances. It's nice to have options, and to think through the pros and cons of each before making a purchase.

The views, information, or opinions expressed in this article are solely those of the author and do not necessarily represent the views of Citizens State Bank and its affiliates, and Citizens State Bank is not responsible for and does not verify the accuracy of any information contained in this article or items hyperlinked within. This is for informational purposes and is no way intended to provide legal advice.